In March 2022, the proposal known as the “Billionaire Minimum Income Tax,” as termed by the White House, was introduced. It is a measure put forth by the U.S. government aimed at gradually reducing the wealth gap. President Biden is urging Congress to enact legislation. Once implemented, the proposal is expected to subject over 700 American billionaires to a minimum income tax of 20%, including currently untaxed unrealized investment income (i.e., investment assets not yet sold). Moreover, the U.S. tax system will become fairer, and over the next decade, the national deficit is projected to decrease by approximately $360 billion.

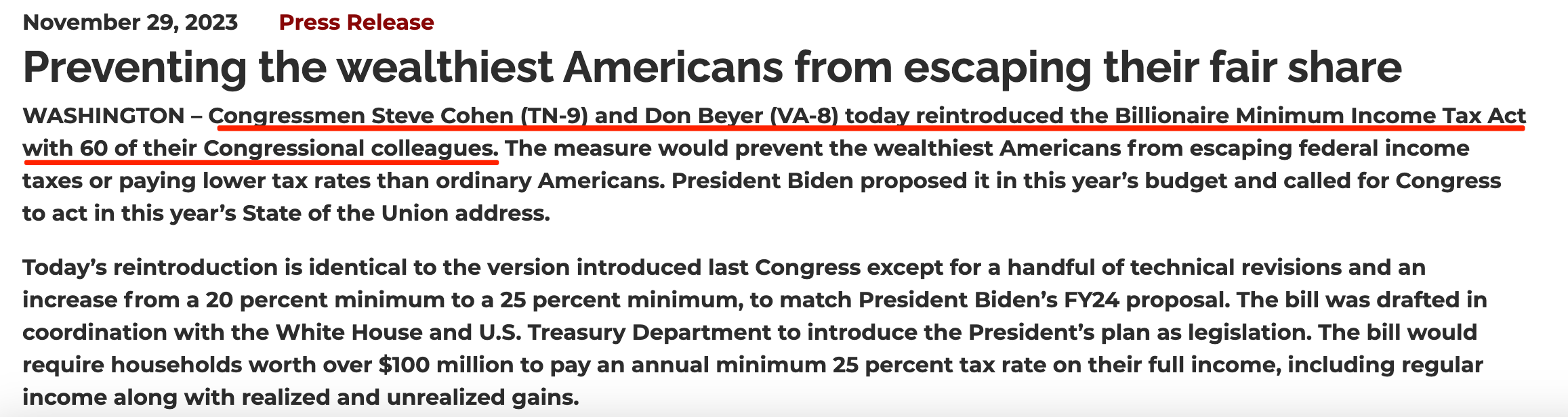

In November 2023, Senators Cohen and Bayer reintroduced the “Billionaire Minimum Income Tax Act,” garnering support from President Biden.

Recently, Biden proposed taxing billionaires once again, proposing a minimum tax rate of 25% for the nation’s 1,000 billionaires, with an expected revenue of $500 billion over the next 10 years. Analysis from reports suggests that the United States is on the brink of passing this legislation, advising high-net-worth individuals to plan their assets in advance.

As the saying goes, “It’s easy to start a business but hard to maintain one.” High tax rates not only cause concerns about the safety of their assets among high-net-worth individuals but also prompt them to plan ahead for the welfare of their future generations. For high-net-worth investors, acquiring a second citizenship is no longer a luxury but a necessity. Opting for a non-global taxation status brings unparalleled benefits to this demographic. Besides offering robust investment portfolios, it provides investors with broader immigration options and visa-free travel, which are crucial for today’s business professionals.

Among European Union countries, Malta stands out as one of the tax-friendly nations with a straightforward tax system. It imposes no gift tax (no taxation on gifts), no inheritance tax (no taxation on inherited property for descendants), no property tax (minimal stamp duty required for property purchases, and no holding tax for property maintenance), and no capital gains tax (no taxation on asset appreciation). While Malta’s corporate tax rate is 35%, it has established a range of financial incentives for Maltese companies engaged in investment and trade activities. Since 1994, the government has implemented a system of partial or full tax refunds for companies, with a seven-year tax exemption period for newly established businesses, taxed at a rate of 5%. Malta has also signed agreements with over 70 countries and regions to avoid double taxation, thereby eliminating the issue of double taxation.

From documents issued by the Maltese tax authority, it is evident that taxation is not based on Maltese citizenship but on the tax residence and the source of income of the individual. This implies that even with Maltese citizenship, investors are not obligated to pay taxes in the country, as most investors do not reside in Malta long-term. Foreign assets and income are sourced elsewhere, thus, as long as income does not originate from within Malta, taxation within the country is unnecessary.

The Maltese passport, renowned for its status as a hassle-free pathway to obtain a highly esteemed European Union citizenship, stands as the epitome of present-day “Golden Passport” programs offering streamlined access. However, under the weight of substantial pressure from the European Union, there are current warnings indicating the impending cessation of the program by 2025. Recognizing that immigration waits for no one, Globevisa advises prospective applicants to promptly submit their applications to seize the limited global quota for EU citizenship. By expediting the application process and positioning themselves preemptively ahead of policy changes, applicants can effectively mitigate any potential impacts that policy shifts may have on their passport applications.

References

https://www.whitehouse.gov/omb/briefing-room/2022/03/28/presidents-budget-rewards-work-not-wealth-with-new-billionaire-minimum-income-tax/

https://cohen.house.gov/media-center/press-releases/congressmen-cohen-and-beyer-reintroduce-billionaire-minimum-income-tax

https://abcnews.go.com/Business/biden-proposes-billionaires-tax-aid-homebuyers-experts/story?id=107880493

https://cfr.gov.mt/en/Pages/Home.aspx

https://legislation.mt/eli/cap/123/eng/pdf

https://cfr.gov.mt/en/inlandrevenue/itu/Pages/Double-Taxation-Conventions.aspx

https://cfr.gov.mt/en/inlandrevenue/legal-technical/Documents/Guidelines%20on%20The%20Remittance%20Basis%20of%20Taxation%20for%20Individuals%20under%20the%20Income%20Tax%20Act.pdf